Gold Mining Scam

Mr. Brost and his team, who called themselves Structurists as they

“structured” their clients’ money,

promised investors annual returns of 18 to 36%.

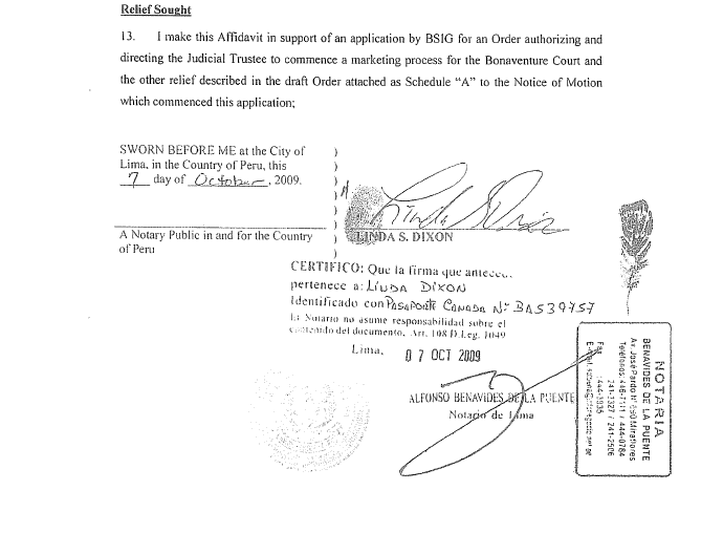

LINDA S DIXON

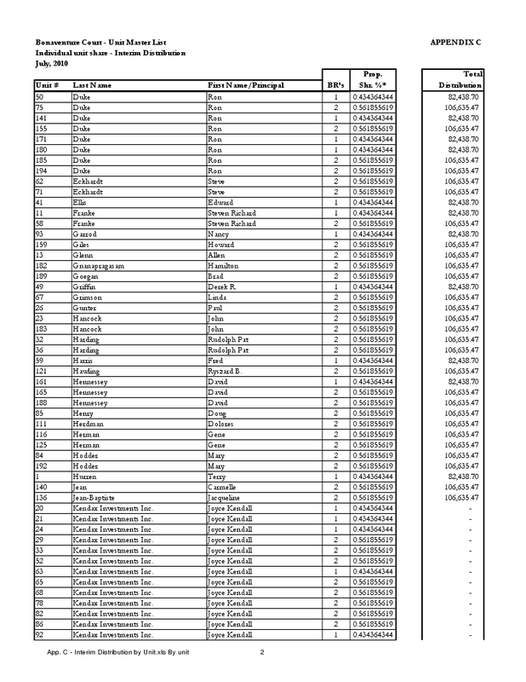

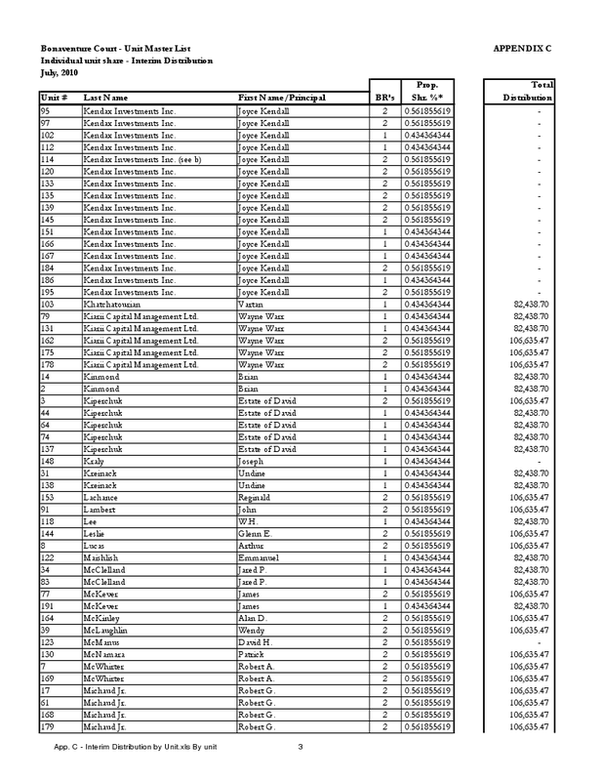

OWNER OF 5 BONAVENTURE COURT UNITS

OWNER OF 5 LIFE INSURANCE POLICIES ON THE ESAY TARGET ESTATE VICTIM

LINDA DIXON

CITY OF LIMA

COUNTRY OF PERU

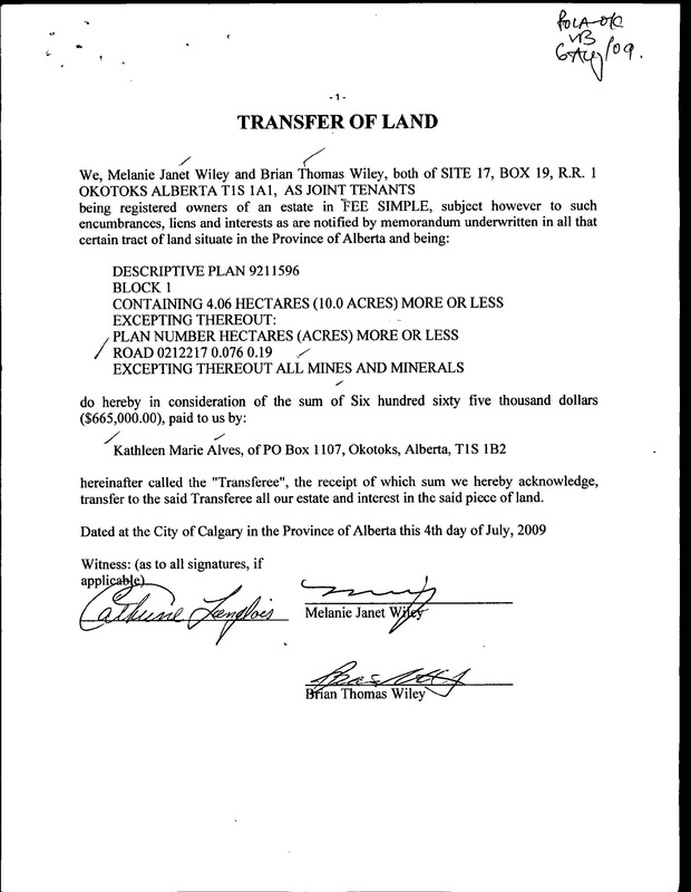

SW CALGARY

BONAVENTURE COURT PONZIE OWNER OF 5 UNITS

Fisheries Minister Shea

Natural Resources, Fisheries and Environment, plus the Prime Minister's Office.

In response to a media call on Oct. 14 about the stock surge that morning, an aide to Fisheries Minister Shea said no decision had been made on the Prosperity Mine.

No one, apparently, was moved to call in the RCMP to investigate a possible leak.

Read more: http://www.cbc.ca/canada/story/2010/11/24/f-greg-weston-taseko.html#ixzz16KwfNEcQ

In response to a media call on Oct. 14 about the stock surge that morning, an aide to Fisheries Minister Shea said no decision had been made on the Prosperity Mine.

No one, apparently, was moved to call in the RCMP to investigate a possible leak.

Read more: http://www.cbc.ca/canada/story/2010/11/24/f-greg-weston-taseko.html#ixzz16KwfNEcQ

Circuit Judge Thomas Penick Jr. got handed the case last month after Circuit Judge Susan Schaeffer removed herself. Johnston claimed Schaeffer was biased against him. She said she withdrew so he would not be able to continue using the tactic to thwart hearings. A tougher legal standard has to be met to disqualify a second judge. In his first hearing with Penick, Johnston handed the judge a copy of his judicial oath and warned him, "Any ex-parte communications will be considered a violation of your oath." sold.http://www.sptimes.com/2002/07/21/Business/Lemon_of_a_deal.shtml

Among the claims he has made: Anyone who mentions his name without his permission owes him $1-million plus damages. Guy Rasco, Davisson's lawyer, says Johnston has sent him bills for more than $100-million already.

Johnston also says the bankruptcy court, which created the trust suing him, has no jurisdiction in Florida. He even tried to claim authority to dismiss the claims against him by incorporating his own company using the First American trust's name. "It is so preposterous," Rasco said. "It's like somebody filing for the fictitious name Warren Buffett and then trying to sell Berkshire Hathaway," he said. "It a total sham."http://www.sptimes.com/2002/07/21/Business/Lemon_of_a_deal.shtml

Johnston also says the bankruptcy court, which created the trust suing him, has no jurisdiction in Florida. He even tried to claim authority to dismiss the claims against him by incorporating his own company using the First American trust's name. "It is so preposterous," Rasco said. "It's like somebody filing for the fictitious name Warren Buffett and then trying to sell Berkshire Hathaway," he said. "It a total sham."http://www.sptimes.com/2002/07/21/Business/Lemon_of_a_deal.shtml

It's not surprising that Johns, 65, is upset. When he cashed out his retirement plan at GTE Corp., he invested $250,000 in First American notes on the recommendation of a trusted friend. Now all he has to show for nearly 40 years' labor is the $20,000 in payments he has received from the bankruptcy court.

[Times photo: James Borchuck]

David Johnston at a hearing last month in Pinellas County Circuit Court. "My wife and I had planned to buy a little motor home and travel," he said. "This put a stop to that. We should have been a lot more prudent in our investigation." Hundreds of investors, seduced by promises of 9.75 percent interest, are still $59-million short. And the man they blame for their losses, David Allen Johnston, still lives in the lavish lakefront home in Pasco County that investors contend he bought with their money. Most of the money never will be recovered, said Melvin Johns, a Venice retiree who serves on the creditors' committee for the bankruptcy case. What investors want now, he said, is revenge: "They want him put out of business so that he can never do something like this again. They want him to suffer like we've suffered."

[Times photo: James Borchuck]

David Johnston at a hearing last month in Pinellas County Circuit Court. "My wife and I had planned to buy a little motor home and travel," he said. "This put a stop to that. We should have been a lot more prudent in our investigation." Hundreds of investors, seduced by promises of 9.75 percent interest, are still $59-million short. And the man they blame for their losses, David Allen Johnston, still lives in the lavish lakefront home in Pasco County that investors contend he bought with their money. Most of the money never will be recovered, said Melvin Johns, a Venice retiree who serves on the creditors' committee for the bankruptcy case. What investors want now, he said, is revenge: "They want him put out of business so that he can never do something like this again. They want him to suffer like we've suffered."

sold to securitization trusts

ORIGINAL 1988 mortgage altered by law firm

SB- BMO BANK LAWYER

SEC. 404. NOTIFICATION OF SALE OR TRANSFER OF MORTGAGE LOANS. (a) IN GENERAL.—Section 131 of the Truth in Lending Act (15 U.S.C. 1641) is amended by adding at the end the following: ‘‘(g) NOTICE OF NEW CREDITOR.— ‘‘(1) IN GENERAL.—In addition to other disclosures required by this title, not later than 30 days after the date on which a mortgage loan is sold or otherwise transferred or assigned to a third party, the creditor that is the new owner or assignee of the debt shall notify the borrower in writing of such transfer,

HUGE- A Brand Spankin New Federal Statute To Attack Foreclosure Assignment Fraud: MATT WEIDNER Posted on22 May 2010.

Via:Matt Weidner Blog

Buried in The Helping Families Save Their Homes Act of 2009, which the President signed into law yesterday, is an amendment to the Truth in Lending Act (TILA) that calls for a notice to the consumer when a ‘mortgage loan’ is transferred or assigned. The provision appears to be effective immediately, and violations are subject to TILA liability.

SEC. 404. NOTIFICATION OF SALE OR TRANSFER OF MORTGAGE LOANS. (a) IN GENERAL.—Section 131 of the Truth in Lending Act (15 U.S.C. 1641) is amended by adding at the end the following:

‘‘(g) NOTICE OF NEW CREDITOR.— :

the creditor that is the new owner or assignee of the debt shall notify the borrower in writing of such transfer

‘‘(1) IN GENERAL.—In addition to other disclosures required by this title, not later than 30 days after the date on which a mortgage loan is sold or otherwise transferred or assigned to a third party, the creditor that is the new owner or assignee of the debt shall notify the borrower in writing of such transfer, including--

‘‘(A) the identity, address, telephone number of the new creditor;

‘‘(B) the date of transfer; ‘

‘(C) how to reach an agent or party having authority to act on behalf of the new creditor;

‘‘(D) the location of the place where transfer of ownership of the debt is recorded; and ‘

‘(E) any other relevant information regarding the new creditor.

‘‘(2) DEFINITION.—As used in this subsection, the term ‘mortgage loan’ means any consumer credit transaction that is secured by the principal dwelling of a consumer.’’. (b) PRIVATE RIGHT OF ACTION.—Section 130(a) of the Truth in Lending Act (15 U.S.C. 1640(a)) is amended by inserting ‘‘subsection (f) or (g) of section 131,’’ after ‘‘section 125,’’.

Via:

Buried in The Helping Families Save Their Homes Act of 2009, which the President signed into law yesterday, is an amendment to the Truth in Lending Act (TILA) that calls for a notice to the consumer when a ‘mortgage loan’ is transferred or assigned. The provision appears to be effective immediately, and violations are subject to TILA liability.

SEC. 404. NOTIFICATION OF SALE OR TRANSFER OF MORTGAGE LOANS. (a) IN GENERAL.—Section 131 of the Truth in Lending Act (15 U.S.C. 1641) is amended by adding at the end the following:

‘‘(g) NOTICE OF NEW CREDITOR.— :

the creditor that is the new owner or assignee of the debt shall notify the borrower in writing of such transfer

‘‘(1) IN GENERAL.—In addition to other disclosures required by this title, not later than 30 days after the date on which a mortgage loan is sold or otherwise transferred or assigned to a third party, the creditor that is the new owner or assignee of the debt shall notify the borrower in writing of such transfer, including--

‘‘(A) the identity, address, telephone number of the new creditor;

‘‘(B) the date of transfer; ‘

‘(C) how to reach an agent or party having authority to act on behalf of the new creditor;

‘‘(D) the location of the place where transfer of ownership of the debt is recorded; and ‘

‘(E) any other relevant information regarding the new creditor.

‘‘(2) DEFINITION.—As used in this subsection, the term ‘mortgage loan’ means any consumer credit transaction that is secured by the principal dwelling of a consumer.’’. (b) PRIVATE RIGHT OF ACTION.—Section 130(a) of the Truth in Lending Act (15 U.S.C. 1640(a)) is amended by inserting ‘‘subsection (f) or (g) of section 131,’’ after ‘‘section 125,’’.

OLD

NEW

THIS OPENS UP A HUGE NEW AVENUE OF ATTACK AGAINST FORECLOSURE AND

ASSIGNMENT FRAUD!

May 2010. a notice to the consumer when a ‘mortgage loan’ is transferred or assigned.

The provision appears to be effective immediately, and violations are subject to TILA liability.

http://stopforeclosurefraud.com/2010/05/22/huge-a-brand-spankin-new-federal-statute-to-attack-foreclsoure-assignment-fraud-matt-weidner/

“BOGUS ASSIGNEE” shown to be the official grantee of the mortgage and no one including the court clerks ever questioned the bogus assignments’ authenticity.

court clerks ever questioned the bogus assignments’ authenticity official grantee of the mortgage BECAUSE THEY WERE THE.“BOGUS ASSIGNEE” -OFFICIAL GRANTEE

Debt Collector’s Duties

Once subject to the FDCPA, a debt collector must disclose clearly to the debtor that, “the debt collector is attempting to collect the debt,” and, “any information obtained will be used for that purpose.”

The FDCPA also requires that a statement be included in the initial communication with the debtor (or within 5 days of the initial communication), providing the debtor with written notice containing the following:

Once subject to the FDCPA, a debt collector must disclose clearly to the debtor that, “the debt collector is attempting to collect the debt,” and, “any information obtained will be used for that purpose.”

The FDCPA also requires that a statement be included in the initial communication with the debtor (or within 5 days of the initial communication), providing the debtor with written notice containing the following:

- the amount of the debt;

- the name of the creditor to whom the debt is owed;

- the statement that, unless the consumer, within thirty (30) days after the receipt of the notice disputes the validity of the debt or any portion thereof, the debt will be assumed to be valid by the debt collector;

- the statement that if the consumer notifies the debt collector in writing within the thirty-day period that the debt or any portion thereof is disputed, the debt collector will obtain a verification of the debt or a copy of the judgment will be mailed to the consumer by the debt collector;

- a statement that upon the consumer’s written request within the thirty day period, a debt collector will provide the consumer with the name and address of the original creditor, if different from the current creditor

Prohibitions against False and Misleading Representation

Under §1692(e) a debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section:

(1) The false representation or implication that the debt collector is vouched for, bonded by, or affiliated with the United States or any State, including the use of any badge, uniform, or facsimile thereof.

(2) The false representation of--

(A) the character, amount, or legal status of any debt; or

(B) any services rendered or compensation which may be lawfully received by any debt collector for the collection of a debt.

(3) The false representation or implication that any individual is an attorney or that any communication is from an attorney.

(4) The representation or implication that nonpayment of any debt will result in the arrest or imprisonment of any person or the seizure, garnishment, attachment, or sale of any property or wages of any person unless such action is lawful and the debt collector or creditor intends to take such action.

(5) The threat to take any action that cannot legally be taken or that is not intended to be taken.

(6) The false representation or implication that a sale, referral, or other transfer of any interest in a debt shall cause the consumer to--

(A) lose any claim or defense to payment of the debt; or

(B) become subject to any practice prohibited by this subchapter.

(7) The false representation or implication that the consumer committed any crime or other conduct in order to disgrace the consumer.

(8) Communicating or threatening to communicate to any person credit information which is known or which should be known to be false, including the failure to communicate that a disputed debt is disputed.

(9) The use or distribution of any written communication which simulates or is falsely represented to be a document authorized, issued, or approved by any court, official, or agency of the United States or any State, or which creates a false impression as to its source, authorization, or approval.

(10) The use of any false representation or deceptive means to collect or attempt to collect any debt or to obtain information concerning a consumer.

(11) The failure to disclose in the initial written communication with the consumer and, in addition, if the initial communication with the consumer is oral, in that initial oral communication, that the debt collector is attempting to collect a debt and that any information obtained will be used for that purpose, and the failure to disclose in subsequent communications that the communication is from a debt collector, except that this paragraph shall not apply to a formal pleading made in connection with a legal action.

(12) The false representation or implication that accounts have been turned over to innocent purchasers for value.

(13) The false representation or implication that documents are legal process.

(14) The use of any business, company, or organization name other than the true name of the debt collector’s business, company, or organization.

(15) The false representation or implication that documents are not legal process forms or do not require action by the consumer.

(16) The false representation or implication that a debt collector operates or is employed by a consumer reporting agency as defined by section 1681a (f) of this title.

Remedies

If the debt collector is in violation of the FDCPA, he/she may be held liable for: (1) any actual damages sustained by the consumer (including damages for mental distress, loss of employment, etc.), and, (2) such additional damages as the court may allow, but not exceeding $ 1,000.

In the case of the class action, the court may award up to $500,000 or one percent of the debt collector’s net worth, whichever is less.

Conclusion

Evidently some advocates believe that without the FDCPA and its provisions which prohibit misrepresentation and deceitful conduct by debt collectors, homeowners as a class have little or no recourse against banks that choose to lie, cheat and defraud the court, while aided by judges who are complicit in the fraud for turning a blind eye and rubber stamping Orders. However, borrowers may have various other causes of action individually, which may or may not be economically feasible to litigate. As always the best advice is to have the loan file audited by a skilled forensic loan auditor to detect violations of federal and state laws followed by consultation with a seasoned foreclosure defense attorney.

Dean Mostofi

National Loan Audits

301-867-3887

Under §1692(e) a debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section:

(1) The false representation or implication that the debt collector is vouched for, bonded by, or affiliated with the United States or any State, including the use of any badge, uniform, or facsimile thereof.

(2) The false representation of--

(A) the character, amount, or legal status of any debt; or

(B) any services rendered or compensation which may be lawfully received by any debt collector for the collection of a debt.

(3) The false representation or implication that any individual is an attorney or that any communication is from an attorney.

(4) The representation or implication that nonpayment of any debt will result in the arrest or imprisonment of any person or the seizure, garnishment, attachment, or sale of any property or wages of any person unless such action is lawful and the debt collector or creditor intends to take such action.

(5) The threat to take any action that cannot legally be taken or that is not intended to be taken.

(6) The false representation or implication that a sale, referral, or other transfer of any interest in a debt shall cause the consumer to--

(A) lose any claim or defense to payment of the debt; or

(B) become subject to any practice prohibited by this subchapter.

(7) The false representation or implication that the consumer committed any crime or other conduct in order to disgrace the consumer.

(8) Communicating or threatening to communicate to any person credit information which is known or which should be known to be false, including the failure to communicate that a disputed debt is disputed.

(9) The use or distribution of any written communication which simulates or is falsely represented to be a document authorized, issued, or approved by any court, official, or agency of the United States or any State, or which creates a false impression as to its source, authorization, or approval.

(10) The use of any false representation or deceptive means to collect or attempt to collect any debt or to obtain information concerning a consumer.

(11) The failure to disclose in the initial written communication with the consumer and, in addition, if the initial communication with the consumer is oral, in that initial oral communication, that the debt collector is attempting to collect a debt and that any information obtained will be used for that purpose, and the failure to disclose in subsequent communications that the communication is from a debt collector, except that this paragraph shall not apply to a formal pleading made in connection with a legal action.

(12) The false representation or implication that accounts have been turned over to innocent purchasers for value.

(13) The false representation or implication that documents are legal process.

(14) The use of any business, company, or organization name other than the true name of the debt collector’s business, company, or organization.

(15) The false representation or implication that documents are not legal process forms or do not require action by the consumer.

(16) The false representation or implication that a debt collector operates or is employed by a consumer reporting agency as defined by section 1681a (f) of this title.

Remedies

If the debt collector is in violation of the FDCPA, he/she may be held liable for: (1) any actual damages sustained by the consumer (including damages for mental distress, loss of employment, etc.), and, (2) such additional damages as the court may allow, but not exceeding $ 1,000.

In the case of the class action, the court may award up to $500,000 or one percent of the debt collector’s net worth, whichever is less.

Conclusion

Evidently some advocates believe that without the FDCPA and its provisions which prohibit misrepresentation and deceitful conduct by debt collectors, homeowners as a class have little or no recourse against banks that choose to lie, cheat and defraud the court, while aided by judges who are complicit in the fraud for turning a blind eye and rubber stamping Orders. However, borrowers may have various other causes of action individually, which may or may not be economically feasible to litigate. As always the best advice is to have the loan file audited by a skilled forensic loan auditor to detect violations of federal and state laws followed by consultation with a seasoned foreclosure defense attorney.

Dean Mostofi

National Loan Audits

301-867-3887